September 2024: I’m looking at a ninety-five-year-old man right now. He is sitting across the room from me. He was born before the stock market crash of 1929, before the Great Depression. Before World War II. Calvin Coolidge was President when Dick Noyes drew his first breath. Beth, my wife of 49 years, is his daughter.

In an early episode of The Beverly Hillbillies, which first aired on television in 1962, Jed Clampett comes into the kitchen — I think it was at the cabin in the Ozarks, but I could be wrong — and he tells Granny that Mr. Drysdale told him they’re going to pay him in some new kind of dollars. Grannie scoffs and says: “There ain’t no new kind of dollars.” Jed turns to Jethro and asks: “What’d he call them, Jethro?” Jethro replies: “Mill-ee-on dollars.”

What we have, compared with 1962, is a new kind of dollars, but the effect is quite the opposite of what it was for the Clampett family.

It is now the autumn of 2024 and my father-in-law is still breathing. Herbert Hoover had not yet been inaugurated President when this old fellow was born. Automobiles were still being built with wooden wheels. Adolph Hitler had not yet been appointed Chancellor of Germany.

And I’m here looking at a person who was breathing the same air as New York’s newly-inaugurated governor, Franklin Delano Roosevelt. Dick would be four years old before Roosevelt assumed his first of four terms as President.

GOLD IN OUR POCKETS

There are U.S. gold coins stamped with Dick’s year of birth. That’s how recently people still owned their own wealth, whether they stored it in a secret place at home or stored it in a commercial bank — effectively lending it to a bank at interest — it was their money, their wealth, their property.

If you had a few dollars back then, (a few dollars had a lot more purchasing power than today), and if a bank held any of it for you, you could accept gold certificates or silver certificates in exchange. At any time, though, you could demand — (“payable to the bearer on demand”) — the certificates’ stated value in gold coin. Or in silver — the bank was flexible.

This occurred during the lifetime of the man across the room who is still living. Breathing. In fact, in February 2021, he was skiing at Maine’s Sugarloaf Mountain. (He also spends a couple months in winter near Loon Mountain in New Hampshire.)

BANKING

The bank that held your gold back when Dick Noyes was a child paid you interest, as I’ve said, for the privilege of using your gold while you didn’t need it. As recently as the 1950s and 1960s, until I was well into my teens, I had a passbook savings account at a local bank that paid 5¼% to 5½% interest. A bank recognized that it was still borrowing money from me.

A bank like that, back then, pooled the savings of little people like me and loaned it to borrowers at a higher interest rate, say 8%, for purposes a borrower might have such as a mortgage or automobile financing. The difference between the bank’s 8% lending rate and the 5% or so that it paid to borrow it from me was how the bank paid its expenses and still made a profit.

But I was a child then, and that was too much interest for banks to pay to children and people like my parents, who were school teachers, in the opinion of big bankers and congressmen, who openly coveted the money that little people were earning. If a bank was making enough profit to share that much with its lenders, including me, it should be those with power, not those with passbooks, cashing in.

It took a few years. It wasn’t until 1961 that a fixed-rate time certificate, a certificate of deposit as we now know it, was established, (although versions of the CD had been around for hundreds of years). Certificates of deposit were paying close to 20% in the late 1970s and early 1980s, earning more than passbook accounts because theoretically banks can loan only the money they have in assets. CDs entice customers to leave their money in the bank for reliably longer periods, making a baseline of assets more predictable. The interest paid is the bank’s cost for the money it lends to its borrowers.

Banking is the one “industry” exempt from and expected to act contrary to anti-trust laws. Conspiring with competitors to fix rates across the industry, to assure profits for all the industry’s members, is something that every other industry would love to do — after all, who doesn’t want to run a company that can’t fail?

The people in power back in the 1960s and 1970s also realized that, if they could re-write regulations — and they did, then instead of letting banks pay you interest for lending them your money, as had been happening, banks could henceforth keep the profits, from lending it to others, and charge the small account-holders for the banks’ “services.” After all, they take the trouble of tabulating your money and keeping it “secure” from everyone (except the federal government’s option to seize it).

Today, we still receive a fraction of a percent in “interest” on the money we lend the banks when we keep it in savings accounts — an annual “yield” of one to two tenths of a percent, for instance. A savings account with a balance holding steady at around $20,000 throughout the year sees a dividend of about $2.50 a month — a veritable joke.

We also pay never-before-heard-of mystery fees. Any one fee generally exceeds the annual interest on tens of thousands of dollars in an account: account access fee, monthly service fee, hard copy statement fee, inactivity fee, account closing fee, maintenance fee, and wire transfer fee, to name a few. (Never mind the questions that this last one raises — how are wires used in transfers differently than the wires used to connect to the internet, for instance?)

The banking industry is driving us toward an all-plastic, all digital payment system. What do the banks stand to gain from this? When you pay cash, the seller gets every penny that you hand over. When you pay by plastic card, the company that issued the card (loosely, a bank but also any of other bank-like entities) gets 1.3% to 3.4% of the transaction right off the top. The price of the item is the same either way. (More on that in another article.) Yes, but the seller pays that, you say. (See the article here called Invincible Ignorance and make sure that it doesn’t apply to you.) Yes, the seller pays that, but the price of everything in the seller’s store has been raised to include that credit/debit card fee. One way or another, the price of everything in America must include all the costs that go into it, including the banks’ extortion in the exchange, the expense of taxes at each stage of production, and much more.

When the banks soon succeed in persuading Congress to impose a 100% digital, 100% cashless payment system, so that the banks can skim a percentage from every commercial and private transaction that occurs in the country, it will amount to a government mandate that we citizens purchase a service from a private company (the bank). This was already challenged under the Affordable [sic] Care Act. Initially that act required that an individual buy insurance or face a penalty. The Supreme Court ruled that the individual mandate was a “tax” and thus a constitutional use of Congress’s taxing power — a use which Congress had not specifically voted to do. Therefore the act was amended to read, in essence: “You must buy insurance, and if you don’t, you shall receive the punishment of a $0 penalty. That’ll teach you!”

That matter has not ended, though. At last reading, as this article from National Review explains, the case has been pushed back to a lower court and there are lawyers graduating from law school today who may be able to make a full, life-long career litigating this one matter.

What’s the point of all this, you ask? Well, in part, it’s to point out that this is your government serving you as you have elected it to do. More to the point, though: It should be instructive for you when Congress eventually decides that you must make all your purchases with a card or other digital representation assigned to you. That will be tantamount to requiring that you buy a service from a private company, in this case a bank instead of an insurance company, and once again Congress will be using its taxing power if it requires you to buy that private company’s service. Maybe this time, though, Congress will come up with a more slippery way to impose the tax — by declaring that banks aren’t entirely “private” entities, maybe? Stay tuned to this one; it will be sickening. With so much money at stake and with the Siamese-twin relationship between Congress and private banks, the banks will prevail, if the whole affair doesn’t first result in fiscal collapse.

PAPER ROUTES

When I was eight and nine years old I delivered the weekend edition of the Toledo Blade on a small paper route in the western Ohio town of Gomer. It was Saturday afternoons when the papers reached me. In wintertime, with an early sunset, I would be out after dark to reach my scattered customers.

I earned a few cents a week. I recall that, at one point, I had four customers stretching from the southwest end of the village, near the turnoff for Ridge Road, to the east end of town, near Pike Avenue just east of Sugar Creek Local School and next to Pike Run, (a tiny Ohio stream made famous in 1939 by Admiral Byrd, explorer of the Antarctic). In a round trip I covered over a mile on foot, often in wind-whipped snow or rain. There were times when I would trudge home through what were probably minor snowdrifts, with frozen tears on my eyelids and with wet feet and frozen bare hands, which was my own fault for setting out inadequately dressed for the weather. It was during such blizzards that I learned the advantages of walking backwards into the wind — I recall it vividly.

Just after Christmas, 1960, we moved the ten miles or so to a house in Lima, where almost immediately I took on a Lima News paper route with around 80 customers. It was an afternoon daily paper that included a Saturday printing and an enormous Sunday morning edition. It took me two trips from my house to deliver all 80 Sunday papers.

From 1961 to 1964, the first three or four years of the seven-year period that I ran that paper route, a subscription cost 35¢ a week. That included the Sunday edition and, of course, home delivery. Those were also the last four years that you could obtain all your money in the form of coin silver, a stable medium of exchange. I walked the route or rode my bicycle, and every Friday evening and Saturday morning I went around to collect each customer’s 35¢, carrying a zippered canvas bag that my belt slipped through.

Each week I collected about $30 — customers often tipped me a little. Other customers who, I knew, were a week in arrears would sometimes argue that they were not behind in their payments, and so I’d settle for what I could get. So it averaged out. What I earned from each subscription slips me now — something around ten cents a week per customer, most likely. That’s around $400 a year.

THE WAYS IT WEIGHS

When Dick Noyes was a kid, 16:1 was the value ratio of gold to silver — 16 troy ounces of silver could be exchanged at a bank for one troy ounce of gold. With any new design of a U.S. coin the weight was seldom changed, so generally the silver dollar contained at least ¾ of a troy ounce of pure silver and a $20 gold piece at about one even troy ounce.

A $20 bill or 20 silver dollars would buy you a $20 gold piece — 0.966 of an ounce of gold. Further back in history the value ratio of silver to gold for centuries averaged about 17:1.

[In late 2025, by the way, with gold at just under $4400 a troy ounce and silver at $65, and giving the market some freedom to set the relative value, the ratio of 68:1 is four times greater.]

(One ounce avoirdupois, what we think of as a “regular” ounce of something by weight — as in groceries, equals 28.3495231 grams. Sixteen ounces equal one pound avoirdupois or just under 454 grams. A troy ounce, used for measuring precious metals, equals 31.10347677 grams, effectively ten percent more than a regular ounce. A troy pound, however, equals twelve troy ounces, not sixteen, so a troy pound is just over 373 grams. The origins of the troy system and the term used to describe it are lost to history.)

EXECUTIVE ORDER 6102

Franklin Roosevelt was inaugurated President, March 4, 1933. Dick Noyes, the man sitting across the room from me, was four years old. One month later, April 5, 1933, Roosevelt signed Executive Order 6102 under authority of the Trading with the Enemy Act of 1917 as amended by the Emergency Banking Act, which Congress passed five days after President Roosevelt took office. (That, sure as hell, was set up in advance!)

Under threat of a fine up to $10,000 (in 1933 dollars), which meant a fine of five hundred $20 gold coins, or up to ten years in prison or both, E.O. 6102 created a new law, “forbidding the hoarding of gold coin, gold bullion, and gold certificates within the continental United States” and required that all persons must deliver all such gold and gold certificates to the Federal Reserve by May 1, 1933. Did you get that? Everyone in the country had just three and a half weeks to fork over their gold! In exchange they would receive $20.67 per troy ounce in paper money: National Currency, Federal Reserve Notes, or Silver Certificates.

Until E.O. 6102 — during the lifetime of the man I introduced in the beginning and who is still here — until E.O. 6102, every American owned his or her own money. After May 1, 1933, the federal government owned everyone’s money. This, of course, is no different from the tyranny that our ancestors fought the Revolution to escape.

(The Gold Reserve Act of 1934 further enforced the transfer of ownership of all monetary gold to the U.S. Treasury and prohibited exchanging silver or paper currency for gold, deliberately devaluing the dollar. It effectively ended the gold standard for private ownership and allowed the government to directly control the money supply.)

A person in 1933 was allowed to keep only $100 in gold coin as well as certain specified coins of numismatic significance. (You’re thinking: OK, but some weeks after turning in all but $100, one guy might casually and quietly exchange something of value with his neighbors — sell them some hogs or loads of gravel or provide some musical entertainment — and presently he would accumulate another hundred dollars in gold coin. What then? Such is the nature of trying to regulate people who can outsmart the system. In my novel, Cold Morning Shadow, one family makes use of this opportunity.)

Silver was to disappear later, when I was a teenager, but more on that in a while.

The 1933 Emergency Banking Act with its provision to confiscate gold was hustled through Congress on the premise that it would stabilize the banks by preventing the hoarding of gold. It would prevent people who owned something of intrinsic value, however little their hoarded wealth might be, from saving it. It would prevent people from saving their money. It would prevent people in the United States from saving what was rightfully theirs.

Did that sink in?

In 1971 President Nixon closed the “gold window,” ending the option of foreign governments to exchange United States dollars that they held for gold from our treasury. Former member of Congress, Ron Paul, explained the consequences of this in this article for the Mises Institute.

WHAT IS MONEY, ANYWAY?

For at least 5,000 years, anything to which a local population ascribed value, which could be carried about comfortably and easily safeguarded, and which would not deteriorate too quickly, served as a medium of exchange — as money. In time, precious metals replaced most other commodities. The difference in value between gold and silver was due to the perceived relative scarcity of each and due to any one metal’s usefulness for ornamentation and so on. Units of gold and silver as well as a few other precious substances could buy just about anything available in any culture, in any time.

Money today is a government’s representation of a medium of exchange. Currently no government permits anything of value to fill that role. Instead, every country uses a substitute, also called “fiat” money, meaning simply that a ruler has declared that the paper certificate fills a void. Fiat money does not have intrinsic value or inherent utility. (There are better materials for stuffing a mattress.)

A fiat is informally defined as a gap, a void, a crack. It is also a declaration by a ruler — a dictator, a king or queen, a president. Fiat money, by decree, creates a void by removing what works and replacing it with a substitute. Incidentally, Fabbrica Italiana Automobili Torino gives us the letters for the FIAT automobile — no relation to the declaration that confiscates the gold and fills the void with the paper.

In the worst case, fiat money is not backed by a commodity that has value, such as gold. That, in fact, is where most of the world stands today. Debt and unfunded promises far exceed any government’s resources in precious metals or other solid commodities to back its currency — and let us not forget that what a government actually does hold in precious metals has been confiscated from the people who, in a free world, would individually own and hold quantities of the substances that serve as their media of exchange. A government pretends to guarantee the constant value and stability of its money but mainly on the strength of that government’s assurances and reputation. The word, fiat, suggests something filling the gap by decree: “It is what I say it is because I am your ruler and I say so.”

In the years since Franklin Roosevelt’s Exectutive Order 6102, there is nothing to distinguish our rulers today from the stereotypical kings of the past who seized, sat on, and squandered the people’s gold. There is little, indeed, to distinguish gold stored underground at Fort Knox, where it is proverbially held, (and which belongs to us), from gold that has not yet been mined from underground veins (only to be stacked in underground vaults). It’s just as unavailable either way.

WHAT, THEN, IS A MEDIUM OF EXCHANGE?

A medium — a commodity or quantity of items that serves as a substance of agreed-upon value — is useful in conducting commerce or trade (exchange) between individuals or groups or countries. Without it, a farmer would need to push a wheelbarrow full of wheat to town to buy a knife from the blacksmith, provided the blacksmith was in need of some wheat. A blacksmith would need to carry some iron implements around that he hoped he could exchange for shoes to fit his children or to obtain coal for his forge. A shoemaker would need to carry an assortment of boots everywhere to trade for furniture. A furniture-maker… well, let that be enough. If each one can carry a quantity of something else, something small — units representing value that also have intrinsic value, then their exchange of goods can be expedited.

It must be acknowledged that all through history, until the present day, human slaves have been bought and sold and traded as if they are money — by countries, large landholders, royalty, and others who are answerable to no higher human authority than themselves. Thus, even today, human traffickers in countries torn by endless civil strife corral people to sell; all the people of China and Russia are manipulated as slaves; North Korea sells men to Russia to be killed in the conquest of Ukraine. Slaves brought from Africa to North and South America up until the 19th century were not the only example of humans being bought and sold as if they were units of money.

When and how, in our pre-history, humans began using something besides their own handiwork as a medium of exchange, we can only guess. It was an early development in every culture.

WHAT IS INTRINSIC VALUE?

Most of what we look at and handle daily is common and ubiquitous — the air we inhale with gusto if we’ve chosen to live where it’s clean or choke on if we’ve chosen to live where it’s dirty, the water that pelts us from the clouds, the dirt or pavement beneath us, the perishable but renewable things we eat or wear. Anyone can readily obtain these things in some form or another with notable exceptions where water is scarce or where political lunacy has caused famines.

Possessing a quantity of air or water or a patch of plain dirt is not at all remarkable.

Apart from these are the more esoteric “things” we can possess such as knowledge, insight, a sense of wonder, and let’s not overlook faith, hope, and love. Anyone can possess these in any measure. We can imbue a remark with knowledge or love, imparting information or hope, but even though these things have value, they cannot be instantly handed over to another person in exchange for goods or services, especially not in constant and visible measure. (I’ve had the pleasure of attending a church, however, which was grateful for donations of “time, talent, and treasure.” At least more than treasure was appreciated.)

Between these possessions lies a class of mostly material things any one of which people universally desire just for itself, for its own sake, for some utility that it has on its own. In some circumstances, knowledge of something important or a unique skill has intrinsic value, but this is not common and universal and timeless. Nor is it readily exchanged for something needed. In some circumstances, clean water (not to mention clean air) has intrinsic value, but it is a substance of fleeting presence, not easily carried about, and who can own it?

Among Earth’s less common resources are a few precious and semi-precious metals and stones. Nothing else has ever quite matched them for desirability, durability, and universal appeal. The ones that have remained most reliably coveted are both scarce and have at least some practical usefulness as well. Soft but durable gold, for instance, has long been shaped into goblets, pounded into foil for gilding, arranged artfully into jewelry, and in more recent times incorporated into electronic components due to its superior conductivity and corrosion resistance.

Among non-metals, diamonds are comparably desirable in both ways, for ornamental uses and for some limited practical applications. Since the quality of individual diamonds varies greatly, a universally-accepted value per unit is not possible. This is not to dismiss the value of quite a few other gemstones and several other scarce metals.

The origins of using materials that have their own intrinsic value, such as these, as a medium of exchange, is lost to history. Humans, stolen from their homelands or captured in wars and subsequently pressed into slavery, have been treated as possessions with intrinsic value as well, although a human slave is not durable in the timeless sense of precious metals.

WHOSE MONEY IS IT?

To be more precise, whose property is it?

In my lifetime the USA has gone off the gold standard and eliminated silver from our coinage. For 5,000 years it has been the individual who owned the medium of exchange in his hand, which for most of that time has been a precious metal. Money with intrinsic value is property. Digital “money” represents property but lacks one key attribute: value. Wealth is a measure of property — a cumulative concept encompassing varied things of value. And since, in the United States, a government cannot own property but can only hold property in trust for its citizens, the question of who owns the money is clear: not your government.

It only prohibits you from holding that property in your own hands and doing with it as you want to.

When money consisted of something of intrinsic value it had nine key properties.

- It was universally valuable in that everyone wanted it — never mind why they might want it — whether for its attractiveness or magical properties or special usefulness in ways other than as money.

- It served as a medium of exchange that practically everyone could agree upon — people would never believe any ruler’s decree that gold was worth less than desert sand or swamp water, for instance.

- You could spend it any way you wanted to.

- It was sufficiently scarce to have steady value and its value didn’t change with whimsical disruptions such as the weather or a change of governing monarchs.

- It was easy to transport discreetly (although vulnerable to thieves).

- It was virtually indestructible where other precious commodities such as dried meat would rot and crystals or dried bread would turn to dust if transported roughly.

- it was a convenient way to store your wealth in a secret place where you could reach it when needed.

- It actually belonged to the person who held it — no other individual and no group even backed by military force could confiscate what they didn’t know you had. Rulers could impose a tax on your assumed wealth, of course, but they could not know your true wealth unless you bragged about it.

- It was private — it was no one else’s business how much you had nor could others, even backed by military force, discover how much you had unless they could coerce or trick you into revealing its amount or its whereabouts.

When the United States first began minting coins in gold and silver in the 1790s, individual citizens would bring their own bullion to the U.S. Mint, there to be tested for fineness and content of precious metal. It was then refined and struck into coinage. (A person did not normally receive the selfsame metal in the form of coinage but an equivalent amount, since it was not practical for a person to wait around until his personal metal was converted to coins. And he received the same quantity in coin that he brought in in bullion. The mint did not keep a percentage as a tax or fee.)

Anyone receiving payment in coin struck by the U.S. Mint was assured by this process that the money was authentic. (Counterfeiters made great strides in imitating real coins early on, though. I do have a convincing-looking counterfeit silver dollar of 1799. But the weight of the coin is wrong, since it was made of another metal.) However, when a citizen brought his precious metal to the mint to be converted into coin currency, who owned the coins thus struck? That money was the property of the individual, not the government.

Did that sink in?

For at least 5,000 years and perhaps two or three times that long, until well into my lifetime, gold has had possessed all of these properties. Silver has as well, but has been more easily obtained and thus not as “precious.”

When our medium of exchange had those nine properties, the unit of currency called the dollar had absolute value, in the tangible sense (as opposed to the mathematical definition of absolute value). In fact, except as technology has affected the performance of such things as electronics and certain manufacturing techniques, what you could buy with, say 20 silver dollars in my childhood you can still buy with 20 (average, well-worn, non-numismatic) silver dollars today, if you’re dealing with someone who understands the value of silver — a Marlin lever-action hunting rifle, for instance, a pair of new car tires, two cords of firewood cut and split. Twenty silver dollars today can buy, in some stable commodities, exactly what $20 would have bought three-quarters of a century ago. But, with silver at over $60 an ounce, it would take about $900 in today’s devalued dollars — today’s fake/fiat money, to buy what that $20 in silver coin would have bought — and still can buy from people willing to accept silver as money. (Some people I’ve dealt with have taken old silver coins from me and have charged the prices you would have paid in those olden days.)

The federal government of the U.S., from its founding, has had the responsibility to coin money, not because the government owns the money, but because the federal government could achieve three things that could not be done reliably by amateurs: It could assure the consistency of the alloys used in coins, it could assure the content by weight of each coin, and it could produce the intricacy of design in coinage that could not readily be duplicated by amateurs.

The federal government did not mess around much with paper currency until the early part of the Civil War. Until then, citizens could accept any form of a promise-to-pay, of course, whether written by a friend on a scrap of paper or printed by special printing presses for a bank, with fancy script and engraving. Some cities and states dabbled in issuing their own currency as well. And so bank notes, checks (remember travelers’ cheques?), and other scrip was around.

And it is entirely legal, if closely monitored, for entities other than the federal government to issue money of some sort, from mass-transit tokens to store coupons to Disney Dollars to IOUs.

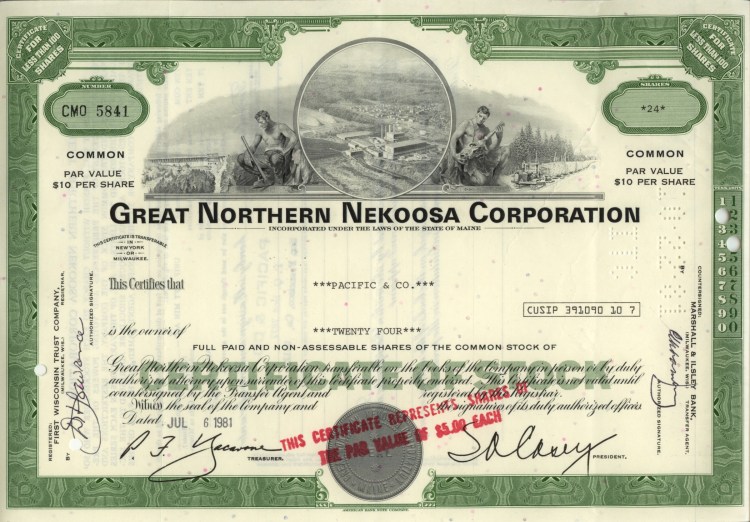

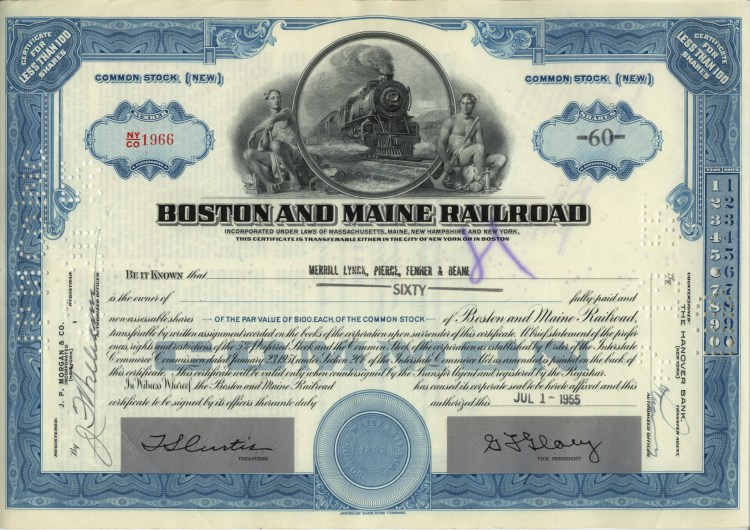

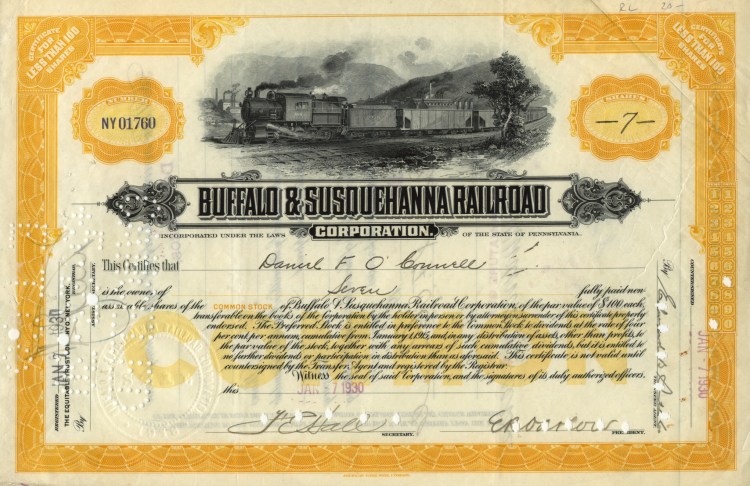

Wealth, however, belongs to individuals, or to groups of individuals in portions they regulate among themselves. An example of the latter are stocks in private corporations. Before the computer age certificates of stock ownership were works of art. Like a gold certificate, a stock certificate represented a portion or measure of the property behind it, (a designated number of “shares”). [Scroll sideways through these five examples.]

THE DAMAGE

In 1933, in an act of singular and sudden impact on history, Franklin Roosevelt and the Congress of the United States swooped in and strangled the arteries of commerce until the lifeblood of private exchange flowed to a trickle, and that was only the trickle of privilege that will always exist for special people.

The lifeblood was the medium of exchange itself, chiefly the gold. When the United States suddenly confiscated what its rulers hoped would be almost all the nation’s gold, what did other countries do within their own borders? Since gold no longer flowed within the USA, it certainly would not be flowing from the USA either in the pockets of travelers or the strongboxes of traveling businessmen. Nor would other countries receive gold for goods sent to the U.S. What gold might be transferred from government to government would henceforth be neither known to nor under the control of any country’s citizens. And so, everywhere else, similar decrees became necessary, whether the people of any other country wanted to continue using gold as money or not. Some countries did for a while longer.)

Now, central banks of nebulous definition swap gold around between countries in order to “stabilize” a country’s fiat currency. If you were to try to discover the amount of gold now owned by your government, which you are not allowed to own yourself — including the gold supposedly protected from foreigners at Fort Knox and the gold held somewhere by U.S. central banks, you would probably not only be prohibited from finding out but investigated as well as a potential foreign agent.

Before the Federal Reserve Act of 1913 about 7,000 independently-owned banks were scattered around the country. Once the first Federal Reserve bank opened in 1914, a system began to take shape, ostensibly to create a network of central banks under a board of directors who would have sufficient power, benevolent only, of course, to prevent the collapse of small banks in any kind of a crisis.

To get it started, the country was divided into eight to twelve regions, each having its own Federal Reserve city, i.e., San Francisco, Chicago, Atlanta, New York, and so on.

By 1927 — before Roosevelt’s Executive Order 6102, the Federal Reserve bank of New York alone held 10% of the world’s entire store of monetary gold. Even before the Federal Reserve Act of 1913, many who were opposed to it were suspicious of granting that kind of authority to a “money trust” of super-rich and powerful men — at the time represented by just three names believed to be controlling Wall Street, (J.P. Morgan, George F. Baker, and James Stillman).

Could it be that these men and a select few others had influence over Congress and the President? Naaawww, no way…

Perhaps mistrust of such giants of finance was warranted, and changes in the final wording of the Federal Reserve Act may have been somewhat successful in thwarting their manipulations of affairs to their own benefit and their misuse of their own great financial influence. But perhaps, also, the law put too much faith in the honesty of the sort of people who would be chosen to govern the Federal Reserve, who already had the necessary experience to be appointed to such positions of trust. Ideally, a government entity needs to be managed not only by individuals who are cheerleaders for the bureau but also by some who are suspicious of the need for the agency’s existence in the first place. Such an ideal, though, has not guided the selection of the Federal Reserve’s directors.

Better ways to prevent bank collapses may have been proposed following the financial crisis of 1907 and again at the start of the Great Depression, ways to begin insuring the deposits of little people in little banks around the country, but no proposal stood a chance of objective consideration unless it assured that certain powerful people retained control and assured that banks and their owners would become wealthier in the end.

We will never know whether there is a better way, for, in October, 1929, the stock market collapsed, and Dick Noyes was already ten months old.

It’s all ancient history? Did I mention that the man who has seen it all is still with us?

WE HAVE BARELY ENTERED A NEW ERA

With the seizure of gold in 1933 and with the expedient of electronic data processing less than a century later, money has now become imaginary. Wealth, however you might define it, exists at the suffrage of those running the federal banking system. Banks are no more protected from collapse than they were before 1913; the only protected wealth is that held by those who control everyone else’s.

Commercial banks, like the ones that offer mortgages and car loans and savings accounts, now have no assets. There is nothing of intrinsic value stacked in their vaults. If a bank even has a vault, it contains only bundles of fiat money — paper. Soon, even this will be eliminated. A bank today is only an arm of the federal government, a contractor of sorts, charged with assisting the government in keeping tabs on everyone’s shares in the country’s foggy nothingness called money. A bank’s “assets” these days are not stacks of real money but mountains of debt. They buy and sell debt. (It may be best not to even try to wrap your mind around that.) Yes, they also have claims (liens) against probably half the personal property and real estate in the country. But there is no longer any basis for the concept that a bank is taking care of your money for you. Because it’s no longer yours, and it’s no longer money.

Perhaps there is a better medium of exchange than precious metals which have the eight key properties listed earlier, properties that precious metals have satisfied until now, though. Maybe there is a substance which the world has at its disposal but has never tried. We, the living, will never know that, for our world is currently under so much surveillance that nothing else can be tried. That is, if a few innovative people were to propose and attempt to use some commodity besides imaginary money — paper currency and cryptocurrency being entirely imaginary and intrinsically worthless — if a few innovative people were to begin using a new, solid, non-imaginary medium, or if barter became widespread as a substitute for fiat money, that activity would eventually be reported to or noticed by the Internal Revenue Service, and the activity would be stopped. (The IRS has already interfered with small-scale barter when it has popped up from time to time.)

Under the current definition of money, the numbers after the dollar signs in your on-line bank and credit union statements are as solid and as private as fog. Visible, yes. Moveable, yes, also as ephemeral; it can all vanish in an instant of data sabotage or government decree. The numbers attached to your name are public; federal inspectors and regulators (“the people” as prosecuting attorneys fondly refer to the government) can look at your account balance and activity on a pretext. And it is seizable; you can be locked out or wiped out at the whim of a bureaucrat or a judge or a data saboteur. All eight of the key properties of real money are missing from the fiat money, digital dollars, and cryptocurrency of the present, but, crucially, the last two: belonging to the person who holds it, and being private.

AFTER GOLD

From 1933 until 1964 a dollar was essentially defined as three quarters of an ounce of silver — an ounce minus the government’s share you might say. (The lower denominations of coinage minted in silver — the half dollar, quarter, and dime, are proportionally smaller: a half dollar contained just over three eighths of an ounce and so on.) From the time my parents moved us to Lima in 1960, when I was ten, right through the year 1964, I was going into the branch bank that stood along my paper route, passing a $5 bill (not necessarily a silver certificate) or a few ones across the counter, and exchanging them for those large, round, silver dollars minted up until 1935. Even then the bank was dispensing them with dates going back to 1878. I still have many of the ones I obtained that way as well as a good deal of other small change from the period.

Silver dollars in circulation were well worn and not desirable to serious coin collectors. As a child, though, I collected coins of any condition in Whitman folders. I still have some of that small change, including the Lima News coin bag shown here, still full of coins of the era.

Dimes, quarters, and half dollars had been struck in U.S. coin silver (0.900 fine) from the earliest mintage in the 1790s. Production of silver dollars was suspended after 1935, until the large Eisenhower dollars were minted from 1971 to 1978. These coin, still an inch and a half in diameter like their silver counterparts up until 1935, were struck in silver for those who could afford them if they even knew about them, and in a nickel-clad bronze (copper) version for circulation, but of course these were mostly hoarded, because everyone thought they must be valuable, until the Susan B. Anthony dollar was introduced in 1979 (and last made in 1999). The SBA dollar was, at last, a subtle nod to the devaluation of the dollar over the previous 122 years: It essentially has the same size and metal content as the United States one-cent copper piece of 1857 and earlier. (See A Tour of Our Recent Coinage below.)

Dimes and quarters were made of silver until 1964, but they were stamped from different, cheap nickel-clad bronze planchets beginning in 1965. From 1965 until 1970 the alloy for half dollars was reduced from “coin silver” (90% silver) to 40% silver, so they still looked silverish and didn’t have that brown ring around the edge that you see on modern quarters and dimes. A quarter today may contain about eight cents worth of metal if treated as scrap.

THE VANISHED HALF DOLLAR

President John F. Kennedy was assassinated in November, 1963. I was 13 and sitting in Miss Whitling’s seventh grade math class when the announcement was made over the loudspeakers at the end of the school day. Here is that afternoon’s Lima News that I have saved ever since that day. For 1964, at the direction of Congress, the Bureau of the Mint replaced Ben Franklin on the silver half dollar coin with an image of Jack Kennedy. In 1964 the Mint issued more than 281 million Kennedy half dollars — still in coin silver as were the 1964 quarters and dimes.

When the half dollar was reduced to 40% silver in 1965 and the rest of our coinage went to the “clad” composition, people began to realize that the 1965-1970 half dollars still had some intrinsic value while the rest of that year’s coinage did not. So people, starting with a savvy few, gradually began stockpiling their silver coins. Some Indian-head pennies were still in circulation as well as coins of the Barber design — silver dimes, quarters, and half dollars, also buffalo nickels, and other older varieties. I was young but I understood and had already been squirreling every strange coin I had found while making my rounds. I still remember showing my parents a strange piece of change now and then.

There were news stories in those days attempting to explain the difference — that the halves would still be made partly from silver until further notice, while the rest would not. Confused, everyone who acquired half dollars from that point on kept them, unsure of which ones retained value. People began hoarding lots of them, jars of them, coffee cans full of them.

Franklin and Walking Liberty halves disappeared from circulation overnight, not gradually as older designs are wont to do when a new piece is introduced. But people also kept all Kennedy halves released into circulation from year to year, right through the 1970s and 1980s and up to the present — if they even see one at all. More than two billion “clad” Kennedy halves have been minted. Most have been released by the Mint to the Federal Reserve banks. If your local bank doesn’t request any from the regional Fed bank, though, then you’re rather unlikely to get your hands on them that way. For the most part, banks have ceased bothering with them because they simply disappear once they go out the door.

And since people won’t spend them, suspecting that they’re rare or worth more than a few pennies apiece, they will never again show up in circulation.

A SIDE STORY

In 1972 the U.S. Army sent me to Deutschland (West Germany). Being a coin collector and also in touch with history, I took a roll of Eisenhower dollars with me (the “clad” kind, not silver ones), along with a roll of clad Kennedy half dollars. On my second day in-country, as I rode the train from Frankfurt to Augsburg, I discreetly offered an Ike dollar to a German gentleman who had bought lunch for another G.I. and me on the train. (He had just given us each a cigar to smoke after lunch.) He became quite excited to see the coin, and his excitement reached a couple members of the train crew nearby. Within minutes I had swapped most of my coins for a quantity of German money, which at the time, at three Deutsche Marks to the dollar, meant I reached Augsburg with something around DM100 in my pocket.

In 1996 I made a two-week solo trip through Ukraine and western Russia. Again I took a roll of “clad” Kennedy half dollars. On a couple of occasions in each country, after becoming acquainted with one of the natives, I again pulled out one of my coins. (I had been advised before going there that the people love little gifts.) In every instance, they declined it after little more than a glance. (That was OK. At that time, with Russian currency at an exchange rate of around 5,000 rubles (also spelled roubles) to the dollar, they were accustomed to mostly paper money, although coins appeared occasionally. They didn’t recognized Kennedy’s profile on the coin and probably suspected that it was a cheap commemorative medal to pin on your breast of the sort the Russian government is known for distributing on any excuse to reward compliance.)

As I was leaving Russia, though, I had to fill out a form at the airport declaring the amount of money I was taking out of the country. I had taken care not to carry any quantity of dollars while I was there. Instead, I would take withdrawals on my debit card in rubles only when I needed cash. I declared on the form that I was leaving with about 100,000 rubles in paper money, worth about $20. I didn’t declare that I was taking any dollars out of the country.

What’s more, I had bought a pile of old Russian imperial coins from a vendor on the street (and had purchased a few in the Kremlin’s gift shop). These I had counted ahead of time and presumed to enter on the declaration as if the amount was in modern currency. And so the face value of a couple hundred imperial coins, minted before the Russian revolution of 1917, was perhaps 40-50 rubles or about one cent in U.S. money, although back when the coins were issued, before 1917, a dollar and a ruble were both based on about the same amount of silver — and quite a bit of the imperial coinage I was carrying out of the country was in old Russian silver.

These old coins were strewn across the hard panel at the bottom of my duffel bag, under my clothes. When my bag went through the x-ray scanner, though, what should appear near the top of my clothes but a black metal cylinder! The airport security officer unzipped my bag, pulled out the light-ochre paper wrapper that still contained most of the Kennedy halves, and handed it to me. “Open it,” he ordered me in English. I did and pulled out a half dollar, at the same time worrying that I had not remembered to declare that I was taking this roll of $20 out of the country — actually $19; a couple of them were gone by then. The security officer’s face brightened and he asked politely, again in English: “Can I buy one from you?” I told him he could have it! He pulled out a wallet, handed me an American dollar bill, and so I sold him two. Then he waved me through and, within a couple of days, I was literally “home free.” After leaving Russia it didn’t matter how much money I was carrying. I did away with the paper wrapper on the Kennedy halves before boarding the flight, though, and let the remaining half dollars lie on the bottom of my carry-on — my only piece of luggage — for the rest of the return trip.

IS ANYONE PAYING ATTENTION?

Being clear on all the differences since my youth, I continued spending the newer cheap-metal Kennedy half dollars. As I did, over time, I encountered store clerks who did not recognize them, who did not believe they were real, who called the manager,s over and who even rejected them sometimes. I did the same with Eisenhower (Ike) “silver” dollars — full-size dollar coins issued in copper-nickel during the 1970s and fully intended by Congress to be used as legal tender.

But there is a herd mentality that dictates people’s responses to change, arising partly from indifference — they’re too busy with trivial matters to pay attention or care, and partly from ignorance — they suspect that there is no way they’ll ever know enough about a subject like this (or that the little they know is all anyone needs to know), and so they submit to the ukase of their elected leaders, who, they assume, know everything and can therefore be trusted. After a decade of confusion (which did leave some concerned people fuming about the devious devaluation of the dollar), the country adapted to the new, worthless medium of exchange, and by the mid-1970s the transition from money of intrinsic value to 100% fiat currency was accomplished, just as the complete transition from fiat cash to 100% digital money is nearly accomplished, to the benefit of the ruling class who had foreseen the need, from the 1930s, to relieve the people of their personal property — their wealth, however meager.

When a stage magician does this it’s called sleight of hand — he appears to give you an ace of hearts but when you turn the card up and look at it again, you discover that you have the three of clubs. With our money, most people haven’t bothered even to turn the card over. The magician in this case has said: “Wait, I’ll be right back,” and then he has disappeared forever. Our reaction, trusting and waiting, is the behavior that the instigators and elite beneficiaries of the changeover were counting on.

WHAT HAPPENED NEXT

And so, when I was a kid — until I was 14 years old, a dollar was still defined as, because it was equal to, one twentieth of an ounce of gold or three fourths of an ounce of silver. In 1974, President Ford signed an order permitting not just special citizens but ordinary citizens as well once more to own gold. Initially, following this opening, gold could be bought in bullion for $32 a troy ounce. As soon as that happened I bought some gold coins from a coin dealer I knew in Bangor.

Silver was still pretty quiet then. In fact, in 1975 or so, I took a bag of silver dimes, quarters, and half dollars — all common coins I had previously hoarded, of average wear and average dates — to that coin shop. I intended to spend it at face value, along with some paper money, on another gold coin or two. The bag held $55 in silver change; I had counted it. The coin shop owner looked at it disdainfully, then regarded me over his half-lensed reading glasses, and said: “I don’t have the time to count it. Bring me paper money.”

I kept the silver instead — the coins in my Lima News bag, and bought my gold, a little anyway, somewhere else.

Gold climbed quickly from $32 an ounce but was still as low as $113 in 1976. In January, 1980, it spiked to $737 but for the next 25 years it settled back into a range of $250 to $500 per troy ounce. By December, 2005, it crossed the $500 mark, and in September, 2009 it passed $1000 and hasn’t looked back.

[In September, 2024, gold was selling for $2,600 and silver at $31 a troy ounce. At Christmastime, 2025, gold is at $4,500 and silver at $70. These metals haven’t changed in value; the dollar is merely shrinking toward the level of the ruble in Russia in 1996.]

BUT WHAT IS A DOLLAR NOW?

Your government is confusing matters greatly. Since1986 you have had the option to buy, from the U.S. Mint, real silver dollars, newly minted, stamped with the year of issue and the words UNITED STATES OF AMERICA and ONE DOLLAR. Each one declares itself to be one ounce of .999 fine silver. It’s a tenth of an inch larger in diameter than the silver dollars that were in circulation when I was young, but, remember: those contained just over three-quarters of an ounce of silver.

Similarly, coins in the 10¢, 25¢, and 50¢ denominations continue to be minted in coin silver. These are included in special mint sets and proof sets and are intended for collectors and as special gifts for dignitaries and so on. And they are not sold by the Mint at face value!

Along with these, since the 1980s, your government has issued gold coins in one-ounce and fraction-of-an-ounce weights in nominal denominations of $50 (for one ounce) on down to $5 (for one tenth of an ounce). Coins in palladium and platinum are also sold by the U.S. Mint.

The denominations are not the prices of the coins, though. Prices are about double the market value of the metal at the time of sale.

When people could hold their wealth in cloth bags and wooden boxes, the wealth in the country was in the control of the people who owned it… Now a dollar is a “relationship,” a concept, a promise payable in nothing but more promises.

The government advises that these special coins are sold as investments and are not intended as currency (money). But, since their intrinsic value is intact, they are money to anyone who wants to use them as a medium of exchange, without regard for their meaningless denominations of ten cents to $50. I have, in fact, used them for large purchases a couple of times in recent times.

But these are not the coins of the realm. These are not the currency of our wages and salaries, our purchases and our bank accounts. They used to be. Now the Treasury mocks us by offering them as expensive portrayals of what, in my father-in-law’s lifetime and in mine, circulated as our medium of exchange.

When a dollar’s value was set by something concrete and when people, if they so chose, could hold their wealth in cloth bags and wooden boxes at home, the federal government was in a bind. The wealth in the country was in the control of the people who owned it. That frightens and frustrates politicians because, if we had wanted to, we could empty the banks and empty the treasury and possess it ourselves. This was the intent of the founders but is not in our modern big government’s dearest self-interest. (Even the founders counted upon people to keep most of it in banks where it earned interest and where the government could then borrow it and issue bonds to cover the debt.)

Now that it has no concrete foundation, a dollar is a “relationship” (against the fiat currencies of other countries), a concept (it ought to have value), a promise (payable to the bearer on demand — payable in nothing but more promises, that is).

WHY?

The dollar’s current ambiguity is to the government’s advantage in many respects, but perhaps most significantly in its relationship to federal debt and currency devaluation (“inflation”). For each dollar the federal government borrows it will repay later with a dollar that has far less purchasing power.

The one unit of our money that still has intrinsic value, in fact greater than its face value, is a penny minted before 1982 (and some that were struck in 1982 as well). There is a special absurdity in that the copper in a penny struck before 1982 has a melt value of almost four cents per coin.

If I had $100 in my coffee can at home in 1962-1964 — and there were times when I probably did — mainly in silver coins, that $100 would be worth close to $3,100 today, in 2021, just for the silver. (A dollar in silver money held 0.77 of an ounce of precious metal, so the price of a full troy ounce of silver up until 1964 was $1.30.) I was, though, encouraged to “keep it in the bank.” We used the Metropolitan Bank in Lima, so that’s where I had my passbook savings account.

[In 1966, three months before my 16th birthday, I bought a car for $395 — a 1939 Chrysler New Yorker, the very one pictured here. The price of a new one in 1939 was $1,298. It was in splendid original condition and I drove it from Ohio to Maine the following summer when the family moved to my father’s home town of Farmington. That price would be the same as paying $21,300 in 2025 for a 27-year-old car in great condition. This one wasn’t even old enough to be eligible for antique car license plates when I bought it! Current value in the antique car market in 2025 dollars: about $25,000.]

Today I can use the price of an ounce of silver as the approximate rate at which our money has been devalued from the time silver was taken out of our coinage: 0.77 of an ounce of silver, the amount of the metal in a silver dollar, defined $1 in 1964, therefore a full ounce was worth $1.30. Now a full ounce costs $31, so a silver dollar is worth $24 for the silver in it. That just tells me that a dollar was 19 times more valuable then. That’s a pretty good indication of the rise in prices since 1964. Some things can’t be compared outright, though. A pound of corn meal is the same substance as it was 60 years ago, yes. Cars in the early 1960s, though, were pretty bare-bones. Power steering, power brakes, air conditioning — these were options that used to cost extra. Now we pay that extra in the base price of every car. Seat belts came in the mid-1960s. Computers and electronic fuel ignition were unheard of in cars. Even so, the price of a new, well-equipped sedan 60 years ago was around $2,000. Now the price is close to $50,000. A loaf of bread that was 19¢ then can run you over $4 today. See the relationship to the rise in the price of silver? I don’t need to go on.

A TOUR OF OUR RECENT COINAGE

Every coin pictured here, except the large penny and the gold piece (either end of the bottom row), has been in circulation during my lifetime and would have been found in my paper route money bag between 1958 and 1967 or in my pocket since then. In the dollar row the third large dollar coin from the left is a “clad” Eisenhower dollar. The large dollar coin on the right is a 1995 silver dollar that I carry as a pocket piece. On the bottom row, left to right: a U.S. one-cent piece of 1851, a Susan B. Anthony dollar of 1999 which is the same size as an original penny and also made chiefly of copper, a Sacajawea dollar of 2007, and a $10 gold piece of 1910.

Did you notice, by the way, that of the 24 coins pictured together above, nine depict men and fifteen depict women? Altogether we can put names to the images on thirteen of the coins if you count both heads on the Sacajawea dollar. (And yes, Lincoln appears twice among the thirteen.) Four depict American Indians, one man and three women. At least a couple other coin varieties of the early 20th century, not included in this photo, also depict Indians. The Barber designs, (dime, quarter, and half dollar at the left of the middle three rows) in fact depict “Miss Liberty,” although the result is quite masculine-looking. Miss Liberty adorns eleven of the 24 coins pictured. Of the eight men pictured, two did not serve as President.

SO LET’S REFORMULATE OUR MONEY

In the 1790s the smallest denomination of U.S. coinage was the half cent. In the 1850s the half cent was phased out. If the dollar of the early 1960s was worth 50-70 time more than a dollar in 2025, then a penny today is worth less than one-fiftieth of a cent of cent in the 1960s. And a penny was barely useful then. Why, why, did we go on making them by the billions for another 60 years???

It’s no wonder that in 1982 the U.S. Mint began stamping pennies out of copper-plated zinc, a much cheaper metal than bronze (which is an alloy of copper, tin, and sometimes small amounts of other metals or metalloids). The one unit of our money that still has intrinsic value, in fact greater than its face value, is a penny minted before 1982. They’re still out there if you’re inclined to pluck them from your pocket change or stir the penny cup next to a cash register.

But a dollar today can barely buy what you could get for a penny when Dick Noyes was a child. Isn’t it time to eliminate the small denominations?

The smallest coin and smallest fraction of a dollar that can be justified any longer is perhaps the half dollar. Twenty years ago I wrote my representative in Congress and recommended four denominations of coinage, 25¢ – 50¢ – $1 – $2, and paper money starting at $5. (The cost of producing $1 coins, even the Sacajawea — a.k.a. Sacagawea — dollars that were then being promoted, which are durable enough to circulate for decades, is far less than the cost of keeping an equal number of $1 bills in circulation.) Half dollars that have been hoarded, if released to banks at all, could return to circulation and would have value roughly comparable to the half cents of the early 1800s.

Of course, there was no interest in Congress in my idea, and so we’re still being oversupplied with zinc pennies.

THE TRUTH

The last two coins in the preceding photo, the Sacajawea dollar and the $10 gold piece, illustrate the supreme absurdity of our current currency. The Sacajawea dollar has a copper core and is clad in manganese brass (which is 77% copper). In other words, it is not only of the same size but has just about the same copper content as a penny of the early 1850s. (Doesn’t that tell you something?) And it presumes to imitate, in size, color, and subject, a half-ounce gold piece of 100 years earlier — and it calls itself a dollar, the same as the largest coin in the photo, the walking liberty silver dollar, which has been minted in the same years as poor Sacajawea. She would be better honored to adorn the larger coin.

A dollar may not be quite as ephemeral as an evaporating puff of steam or a drifting wisp of fog, but there is little else to compare it to. (A melting block of dry ice?) And that’s how our rulers want to keep it. In each generation, Americans will have a new experience with money, a new scale for the value of a dollar, a new relationship with the next-current medium of exchange.

Old people, such as Dick Noyes, and I, born in 1950, will have our own perspectives, but we won’t be able to make you younger ones grasp it as we do. You can’t relate to it, and, really, you don’t want to hear it. I understand. You don’t have the time. It’s hard to appreciate what it was once like, anyway. And what’s the point of trying to see into the past? There’s no going back. You’re stuck with the government-intrusive fake money of the foreseeable future.

That right there is the truth. There’s only the future, and your complete dependence on government — on the ruling class who sit on the real money and regulate the fiat money while permitting you to fondle a little of it — is being ever more and more assured. The motives of people who insist they must rule you for your own good, those who always want to help you, whether you want their help or not, and who are successfully forcing you to live under their smothering helpfulness, may be pure in original intent. You who elect them to office are mostly — and naïvely — motivated by the desire for happy outcomes. But those who are elected, wanting happy outcomes too, are motivated by the determination to impose happy outcomes. Those people, in every generation, in every government in every country, are the dangerous ones.

The old ways were not necessarily better. Nor were they demonstrably worse in many respects. But the new ways have not done away with the evils of the past — the inequities, the corruption, the hazards, the propensity of some to lord it over others. We still have scammers and thieves. In spite of the expensive, government-run “wars” on drugs and poverty we still have the addicted and the poor and the dishonest and dangerous among us in the same measures as always. We still have the mentally ill, even though we now insist that they must try homelessness and suffer a universal unavailability of services. In the past, many (in the U.S. anyway) were confined against their will — against their right to be a nuisance or a menace everywhere. (The mentally ill were provided housing and services in the not-so-distant past, but see Insane Asylum at DamnYankee.com. Conditions in mental institutions were often atrocious, but then again, so are year-’round conditions in a tent city beneath a railroad bridge on the edge of every city, large and small.)

We still have corruption among regulators and overseers. In both dominant parties we still have politicians owned by labor unions and corporations. We still have price-gouging purveyors of “services.” (Time-Warner/AT&T, I’m talking about you.) Corporations create demand for their products by persuading Congress that such “innovations” as electric cars and windmills are holy, never mind the toll each takes on the environment both in manufacturing its components and in junk left behind when their brief period of usefulness has ended.

So forgive us oldsters for our skepticism. We have been through a few cycles of popular enthusiasm over the same old tricks trotted out in new costumes. We are holding the three of clubs, while you youngsters and idealists and collectivists believe your card is the ace of hearts.

In my novel, Cold Morning Shadow, after remarking on the extermination of real money as discussed here, Henry Clay Comosh poses the question: “Who else gets to see something happen for the first time in five thousand years?” I realize the era has come to an end when humans used a medium of exchange that has intrinsic value. Ending it, though, was so unnecessary. And the replacement for it is so very inadequate.

=David A. Woodbury=

Originally published 30 March 2021, some details updated 20 September 2024 and 16 December 2025

A couple of additional observations:

1) A dollar today has about the purchasing power of a penny of the 1850s, a hundredfold loss of value. A dollar might have bought you a night’s lodging in 1850. Now it takes $100 and more. Granted, the quality of the accommodations has improved. The SBA and Sacajawea dollar coins match the penny of 1851, shown above. Before that decade was over, the country decided that we didn’t need the half cent any longer. If a dollar today is worth a penny of that time, why do we need to break it down into 100 smaller units today?

2) Thinking about inflation, we hear that prices keep going up and up. Maybe we need to rephrase that. Maybe prices have remained steady but we need to say that the dollar keeps shrinking and shrinking — that the value of a dollar keeps falling. That would acknowledge what is truly happening.